ASIAN ENERGY SECURITY STRATEGY 2026–2035

Post-Iran War

Demand Growth, Strategic Vulnerability and the Race for Energy Independence

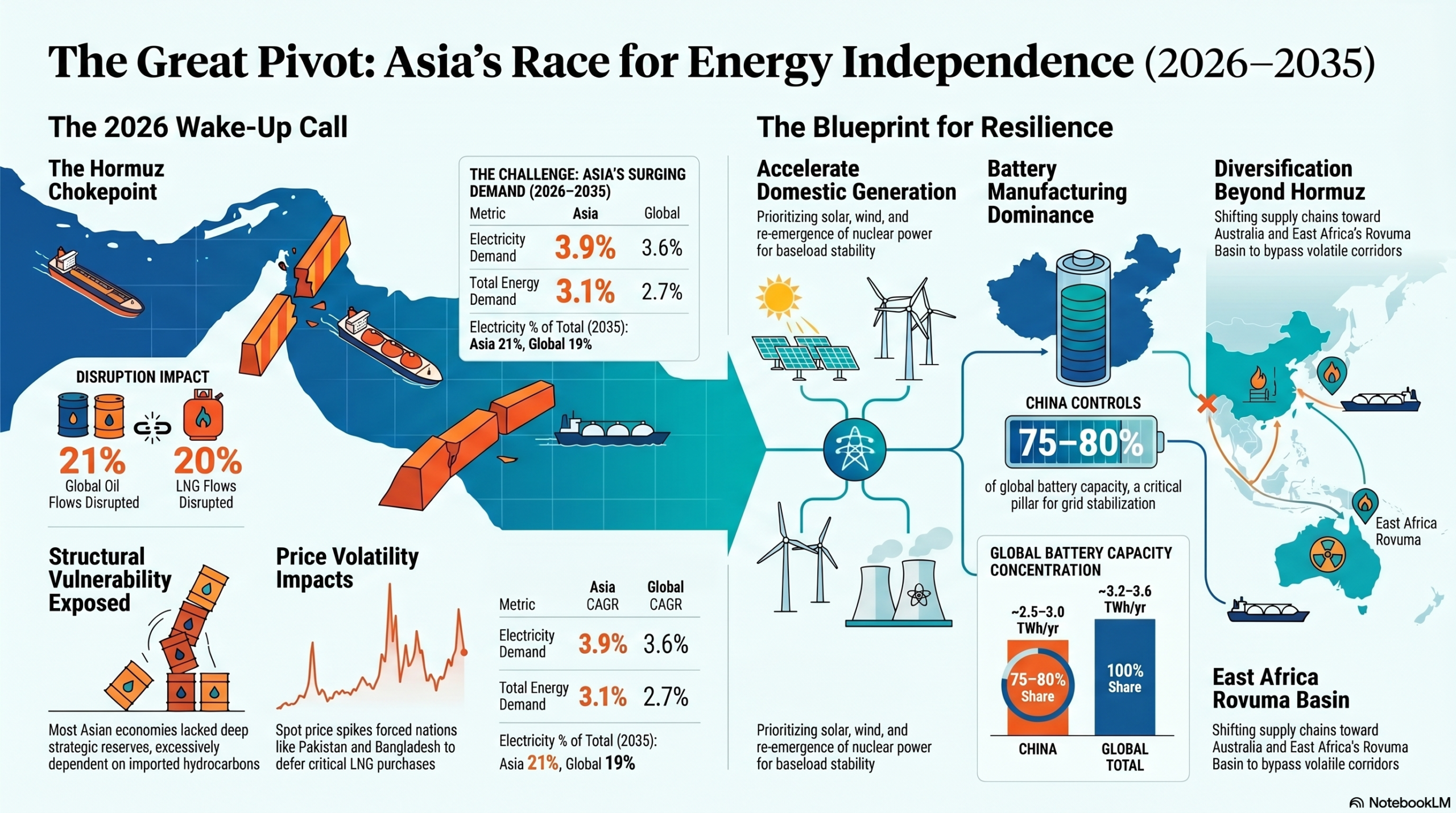

The Iran war of 2026 transformed energy security from a long-term climate and infrastructure issue into an immediate geopolitical priority for Asia. The disruption of the Strait of Hormuz — through which nearly 21% of global oil trade and 20% of LNG flows transit — exposed the structural fragility of a region heavily dependent on imported hydrocarbons despite accounting for most future global energy-demand growth. In this article, we examine Asia’s energy-security landscape through 2035 and argues that the region’s resilience will increasingly depend on electrification, domestic renewable and nuclear deployment, strategic reserves, diversified fuel sourcing and deeper regional integration.

The End of Asia’s Old Energy Model

For decades, Asia’s energy architecture rested on a simple geopolitical assumption: that Middle Eastern oil and gas flows through the Strait of Hormuz would remain broadly stable. The Iran conflict of 2026 shattered that assumption. Following the joint US–Israel military offensive against Iran in February 2026, Tehran disrupted maritime traffic through Hormuz, triggering one of the largest energy-security shocks in recent Asian history.

Oil and LNG prices surged within days. Several Gulf producers invoked force majeure on selected cargoes, while Asian importers scrambled for alternative supply. Bangladesh and Pakistan deferred LNG purchases as spot prices spiked. Larger economies such as India, Japan and South Korea sought emergency cargoes from the United States, Australia and Africa. The crisis revealed that Asia’s vulnerability was not cyclical, but structural.

Three weaknesses became immediately visible. First, the region remains excessively dependent on imported hydrocarbons. Second, most Asian economies lack deep strategic reserves. Third, clean-energy deployment remains insufficient relative to the scale of future demand growth. What had previously been viewed as an energy-transition challenge has now become a strategic-security imperative.

Asia’s Energy Future:

Bigger

More Electric

More Exposed

For decades, Asia’s energy architecture rested on a simple geopolitical assumption: that Middle Eastern oil and gas flows through the Strait of Hormuz would remain broadly stable. The Iran conflict of 2026 shattered that assumption. Following the joint US–Israel military offensive against Iran in February 2026, Tehran disrupted maritime traffic through Hormuz, triggering one of the largest energy-security shocks in recent Asian history.

Oil and LNG prices surged within days. Several Gulf producers invoked force majeure on selected cargoes, while Asian importers scrambled for alternative supply. Bangladesh and Pakistan deferred LNG purchases as spot prices spiked. Larger economies such as India, Japan and South Korea sought emergency cargoes from the United States, Australia and Africa. The crisis revealed that Asia’s vulnerability was not cyclical, but structural.

Three weaknesses became immediately visible. First, the region remains excessively dependent on imported hydrocarbons. Second, most Asian economies lack deep strategic reserves. Third, clean-energy deployment remains insufficient relative to the scale of future demand growth. What had previously been viewed as an energy-transition challenge has now become a strategic-security imperative.

Asia’s challenge is therefore two-fold: meeting enormous incremental energy demand while simultaneously reducing geopolitical vulnerability. The region’s transition is increasingly defined not just by decarbonisation, but by resilience.

Table 1: Asia vs Global Energy and Electricity Demand (fig in TWh)

Electricity % of total energy demand

Diverging National Strategies

China and India will largely determine Asia’s energy-security trajectory, though their approaches differ sharply.

China has built one of the world’s most diversified energy systems. It produces nearly half of global coal output, operates more than 60 GW of nuclear capacity and has scaled renewable capacity to almost 2,000 GW. The country now sources close to half of its electricity from renewables and has aggressively diversified oil and gas imports through Russia, Central Asia, Africa and Latin America. China’s strategy is based on domestic capacity expansion rather than crisis management.

India’s position is more complex. Despite ambitious renewable targets, the country remains heavily dependent on imported crude oil and LNG, with import dependence approaching 90% for oil. Coal will continue to remain central to India’s energy mix for at least the next two decades, even as solar deployment accelerates.

Japan, South Korea, Taiwan and Singapore remain among the world’s most import-dependent economies. For them, diversification, nuclear restarts and long-term partnerships with Australia and the United States are becoming strategic necessities rather than policy choices.

Seven Strategic Pillars for Asian Energy Security

1

Accelerate Renewable and Nuclear Deployment

The most durable solution to import dependence is domestic energy generation. The Iran crisis has accelerated political support for solar, wind, hydro and nuclear power across Asia. China already dominates global renewable deployment, while India has announced one of the world’s most ambitious solar expansion programmes. Nuclear power is also re-emerging as a strategic necessity. Southeast Asia, which historically avoided nuclear energy, is increasingly reassessing its position. Malaysia, the Philippines, Vietnam and Indonesia are all evaluating reactor or SMR programmes as part of long-term energy-security planning. The combination of solar for daytime generation and nuclear for baseload stability could become Asia’s preferred clean-energy architecture.

2

Build Battery and Energy Storage Capacity

Battery Energy Storage Systems (BESS) are becoming central to modern electricity systems by stabilising renewable-heavy grids and reducing fossil-fuel dependence. China currently controls nearly 75–80% of global battery manufacturing capacity and dominates the entire supply chain, from mineral processing to cells and pack assembly. The strategic significance of batteries increasingly resembles that of semiconductors or solar manufacturing. Countries dependent on imported energy may soon find themselves equally dependent on imported battery systems unless domestic manufacturing ecosystems emerge.

3

Diversify Supply Towards Africa and Australia

Asia’s energy diversification strategy is increasingly shifting towards Africa and Australia. East Africa’s Rovuma Basin in Mozambique and Tanzania holds roughly 129 trillion cubic feet of gas and bypasses the Strait of Hormuz entirely. Africa is also becoming strategically important due to its reserves of cobalt, lithium, graphite and manganese — minerals essential to battery and renewable-energy systems.

Australia, meanwhile, has emerged as Asia’s most reliable external energy partner. The country combines political stability with large exports of LNG, uranium, thermal coal and critical minerals such as lithium and nickel. Projects such as Sun Cable — the proposed 4,200-km subsea electricity link between Australia and Singapore — indicate how future Asian energy trade may increasingly involve electrons rather than hydrocarbons.

4

Electrify Consumer Energy Demand

Electrification is becoming one of the most powerful energy-security tools available to governments. Electric vehicles, induction cooking and rooftop solar reduce direct exposure to imported oil and LNG. China’s EV penetration has already crossed 50% of new vehicle sales, while Thailand, Indonesia and Vietnam are introducing aggressive EV targets.

More than 100 million people in Southeast Asia still rely on biomass or kerosene for cooking, creating both health and energy-security vulnerabilities. Large-scale household electrification could therefore reduce fuel-import dependence while simultaneously improving public health outcomes.

5

Expand Strategic Energy Reserves

The Iran crisis exposed the shallow reserve depth across ASEAN and South Asia. Several economies entered the crisis with only weeks of operational fuel inventories. China, by contrast, has built one of the world’s largest reserve systems with an estimated 1.1–1.3 billion barrels of strategic and quasi-strategic storage — equivalent to roughly 180–200 days of net-import cover.

India has expanded its SPR programme, though reserve depth still remains below IEA benchmarks. ASEAN economies remain particularly vulnerable due to limited fiscal capacity and inadequate underground storage infrastructure.

6

Leverage Digital Energy Systems

Energy security is increasingly linked to digital infrastructure. AI-enabled smart grids, demand-response systems and distributed energy management can reduce peak electricity demand by 15–25%, lowering fuel-import requirements during crises. At the same time, AI and cloud infrastructure are becoming major electricity consumers. ASEAN’s data-centre capacity is expected to expand sharply by 2030, creating new opportunities for renewable-linked power purchase agreements.

7

Build an Asian Energy Security Architecture

Asia’s vulnerability is collective rather than national. ASEAN’s long-delayed initiatives such as the ASEAN Power Grid and Trans-ASEAN Gas Pipeline should now be accelerated into binding regional infrastructure projects. Beyond ASEAN, a broader Indo-Pacific energy framework involving Australia, India, Japan and Southeast Asia could coordinate LNG procurement, strategic reserves, critical minerals and renewable infrastructure investment.

China, despite geopolitical tensions, shares the same strategic interest in reducing Hormuz dependence and will remain central to any future regional energy-security architecture.

Conclusion

The Iran war of 2026 accelerated a structural shift already underway across Asia’s energy system. The central lesson is clear: dependence on a single region or maritime corridor is no longer strategically sustainable.

Asia’s future resilience will depend on diversification, electrification, strategic reserves, renewable deployment, digital infrastructure and regional integration. The energy transition is therefore no longer simply a climate issue. It is increasingly a geopolitical, industrial and national-security imperative.

If the urgency created by the 2026 crisis translates into sustained investment and political coordination, Asia could emerge by 2035 with a significantly more resilient and self-reliant energy system.

Great insights as always from Ram, one of the sharpest energy minds in Asia!

Great insights as always from Ram, one of the sharpest energy minds in Asia!

This is an excellent piece nicely describing the key imperative for Asian economy. Can’t agree more with Ram that the Middle East crisis is a lifetime opportunity to reset their energy sourcing and usage systems. Along all the suggestions, country like India must deregulate the oil and gas industry to produce more domestic production to reduce import dependence.

Nice analysis! Lots to think about here. I wonder how timely nuclear power can really be, especially as SMR.